Economist Mark Dotzour Says DFW Home Prices Likely to Rise Over Next 24 Months

Dr. Mark Dotzour, former chief economist with the Real Estate Center at Texas A&M University, says rising inflation will lead to higher home prices in the next few years.

Key Takeaways

- Dallas/Fort Worth home prices are likely to move higher in the next 12-24 months.

- Mortgage rates in the 6.5%-7.0% range are normal and likely here to stay.

- Inflation will likely rise over the next 12-24 months.

- Nearly 6,000 people continue to migrate to DFW each month.

Dr. Dotzour Speaks to Real Estate Professionals

Last week I had the opportunity to attend a one-day conference in which legendary real estate economist Dr. Mark Dotzour gave the keynote address. If you are not familiar with Dr. Dotzour, he is the former chief economist at the Texas A&M Real Estate Research Center. Since retiring 10 years ago, he has gone on to speak at hundreds of symposiums and gatherings all over the world. He conducts detailed research into economic impacts on the real estate market -- especially the Texas real estate market -- and then shares his views and findings with real estate and economic professionals everywhere.

In his address last week at the Old Republic Title Economic Forecast, Dr. Dotzour outlined his current view of the Texas real estate market as well as his view of the overall global economic picture. There are three key points that he made that I want to draw your attention to.

- Current mortgage rates of around 6.5%-7.0% feel high, but they are historically normal. In all likelihood, these rates are here to stay.

- Inflation will likely rise significantly over the next 12-24 months due to higher wages, more government spending, and relatively easy credit.

- Home prices in the DFW metro area will likely rise due to the increased inflation as well as increased demand from migratory patterns.

Current Mortgage Rates Are the "New" Normal

Let's start with mortgage rates.

Before I get into the specifics of Dr. Dotzour's mortgage outlook, let me remind you that mortgage rates are tied closely with the 10-year Treasury note. The bond market can be daunting if you are not used to digesting its movements.

Suffice it to say that the safest investments in the fixed income (i.e. bonds) world are Treasury bills, notes, and bonds (collectively known as Treasuries). If you are an investor looking to put your money on a pretty sure-fire bet, Treasuries is it. This means that for something else to warrant your attention, it has to look better than Treasuries. The only way to do this in the bond market is to offer a higher interest rate than is being paid on Treasuries.

When a mortgage gets created, it eventually gets sold and packaged into investable securities on Wall Street. This is known as securitization. These securities get sold to investors as bonds. Like any other bond, the Mortgage Backed Securities (MBS) can be bought and sold on the open market. When demand is high for the MBS, their prices go up. When their prices go up, their yield goes down because now the cash flow payments coming from the MBS are lower relative to the price the investor purchased the security at.

If this all seems a bit confusing, don't sweat it. Just remember that mortgage rates track the 10-year note because the 10-year note is considered a safer alternative to Mortgage Backed Securities. In other words, when the yield, or interest rate, on 10-year notes rises, the interest rates on 30-year mortgages also rise.

With this in mind, consider the graph above. This graph shows the 30-year mortgage rate in red and the 10-year Treasury note yield in blue going back to 1976. The first thing to note is how identical the two lines look. The red line (the mortgage line) rises exactly when the blue line rises and sinks exactly when the blue line sinks.

The second thing to notice is the green circle I've drawn. Mark Dotzour points out that this time period (from roughly 2001 to 2007) was the last time that mortgage rates were NOT being artifically influenced by the Federal Reserve. Recall that when the financial crisis began in 2008, the Fed began buying MBS in order to assuage the fears on Wall Street that all MBS were bad. The effect of this massive Fed purchase was that the mortgage rates went down.

I've drawn the orange line to indicate the peak of the 30-year mortgage rate during the last non-Fed influenced period. As you can see, once the Fed began buying MBS, the rate went down significantly and stayed that way until 2022 when the Fed began unwinding its purchases by selling them on the open market. This resulted in the sharp increase in mortgage rates that we have all been so familiar with over the last several years and is depicted on the far right side of the graph.

As you can see, to Dr. Dotzour's point, where we are now matches where we were just prior to the Fed starting its massive MBS purchases (known as Quantitative Easing). Dr. Dotzour says where we are now is actually normal. Where we were for nearly 15 years was not. As a result, people will start to get used to current mortgage rates. When that happens, they will not be so reluctanct to buy a house!

Inflation To Rise

The Federal Reserve has a long-stated goal of maintaining 2% inflation as measured by the Consumer Price Index (CPI). This simply means that according to the Fed, they are happy if prices of consumer goods and services are generally rising 2% year-over-year. Not long after they began raising rates in 2022, Jerome Powell (the Fed Chairman) indicated that they would continue to raise rates or keep them level until inflation decreased to the 2% range. At that time, inflation was running over 8%. For some reason, in late 2024, the Fed decided to lower rates even though inflation was still around 2.8%. When the fed funds rate goes down, inflation often rises, especially when the economy is healty. Dr. Dotzour points out that current economic conditions in the US are very healthy, so the odds of inflation rising now that the Fed lowered rates are pretty high.

Add to this the fact that wages are continuing to rise as well. With incomes rising, people have more to spend, and this also adds to inflationary pressure.

Finally, our government is committed to spending enormous amounts of money in the coming years. Our national debt currently sits at over $36 Trillion, and the Congressional Budget Office is forecasting a $2 Trillion budget deficit each year for the next 10 years. All of this debt means that our national interest payments are skyrocketing. This in turn means that the Fed will almost certainly have to continue to print money just to keep up.

What does all this mean? According to Dr. Dotzour, it means that inflation will likely rise significantly in the next 12-24 months. And when inflation rises, home prices tend to rise.

One other point I should mention here. Dr. Dotzour pointed out that rents make up 1/3 of the CPI. Currently, rents are stagnant nationwide due to a glut of apartments. However, as the apartment market normalizes over the next couple of years, rents will start to increase again. This means that that portion of the inflation index (CPI) will start going up and only add to the other inflationary pressures I've just mentioned.

In summary, inflation is almost certainly going to rise over the next couple of years, and when it does, home prices will rise too.

Home Prices in Dallas/Fort Worth Set To Rise

The residential real estate market in Dallas/Fort Worth has been locked up for a couple of years now. By that I simply mean that the volume of homes trading hands has been statistically lower than it has been in nearly a decade. Prices have not gone down. Only the volume of homes selling has gone down. As I've stated many times, the reason for this is primarily because of higher mortgage rates (relative to the last 15 years) coupled with already elevated home prices. Higher property tax burdens and insurance burdens are also contributing to this effect.

However, as people get used to 6.5%-7.0% mortgage rates, they will eventually start buying homes again. According to Dr. Dotzour, when that starts to happen, we can expect to see a more rapid appreciation in residential real estate values.

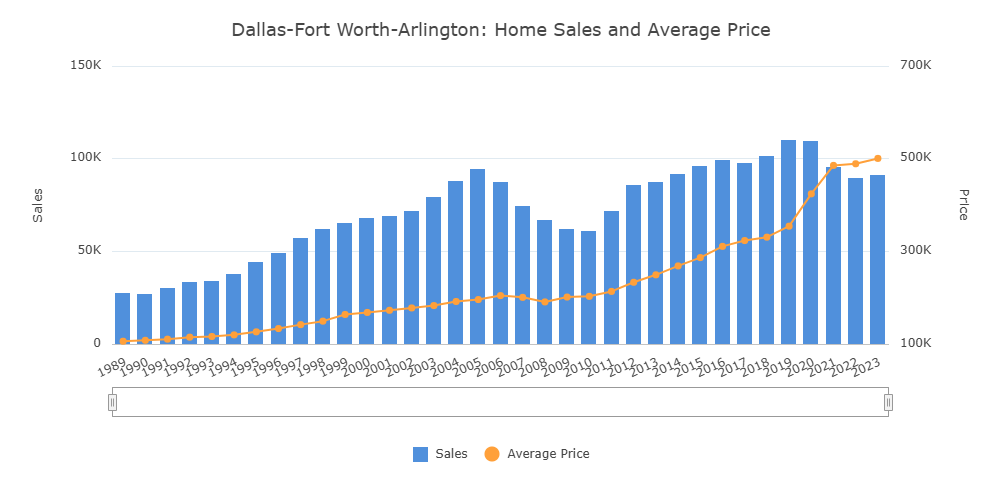

Look at the graph above. Notice that when sales increase, price always increases as well. Sometimes price increases even when sales dip - as has been the case over the past few years. But when sales rise, so do prices. If Dr. Dotzour is right, and I believe he is, we should see significantly higher home prices relatively soon. It might still take a year or so for people to get comfortable with higher mortgage rates, but when they do, they will buy and sell once more.

Additionally, there is the migration factor. I know I state this often in my posts, but it bears repeating. Roughly 6,000 people continue to move to Dallas/Fort Worth every month. These people have to live somewhere. Every one of them adds to housing demand, be it rentals or purchases. This demand keeps a natural floor on home prices. This is why I've said many times over the last several years that home prices are unlikely to decline in DFW.

To summarize, increased demand means increased prices. Housing demand in the metroplex has been relatively low for several years now, but so has supply, and this is why prices haven't moved much. But as inflation rises and people get used to 6.5% mortgage rates, housing demand will increase, and prices will move higher.

Conclusion

Where does all this leave us?

First and foremost. DFW metroplex home prices will go up from here. You can just about bank on that.

I still hear people say they are waiting for mortgage rates to drop and/or home prices to drop before they start looking for a home. The reality is that neither of these things is likely to happen anytime soon. And by that I mean probably in the next 10 years at least. Yes, we could have a black swan event. If we do, all bets are off. What do I mean by that? I just mean we could have another pandemic or a massive war or some kind of rogue terrorist attack or something like that. But barring a black swan event, DFW home prices will almost certainly go up.

Mortgage rates in the 6%+ range are here to stay. Again, a black swan event could precipitate the Fed buying massive amounts of Mortgage Backed Securities again, which would drive mortgage rates down. But barring this, the current 6% range is likely the new (again) normal.

Inflation will also likely rise, and this will only contribute to rising home prices.

If you are thinking or needing to buy a home in DFW, there simply isn't going to be a better time than now. I understand that sometimes we have to wait because we don't have enough saved for a down payment or we are anticipating a family change or something like that. I'm just talking to those who are waiting because they think prices and/or rates are going to go lower. If that's you, you won't have a better time to buy than now.