A Fed Rate Cut Doesn't Mean a Mortgage Rate Cut

I have seen several articles recently indicating that the much anticipated Federal Reserve rate cut in a couple of weeks will lead to lower mortgage rates. While I can't predict mortgage rates per se, I can say that the reasoning behind this belief is flawed.

Key Takeaways

Key Takeaways

- The Federal Funds rate does not directly impact mortgage rates.

- There is a strong likelihood that the recent mortgage rate decline is in anticipation of the Fed's possible rate cut.

- You may be costing yourself if you are putting off a real estate transaction hoping for lower rates in late September.

I have written previously about the true drivers of mortgage rates, so I won't get too deep into the details here. However, I do think it is prudent to summarize mortgage rate influencers once again for the sake of this conversation.

What Drives Mortgage Rates

The first thing to mention here is that the Federal Reserve does not directly set mortgage rates! The Fed is responsible for setting the Federal Funds Rate, which is the rate that banks charge each other for overnight loans. When a bank's overnight rate declines, it means their cost of borrowing cash overnight goes down. This in turn allows them to loan money to the public at slightly lower rates. So, if you own a small business, and you are seeking a business loan, the Fed's actions will likely directly impact your cost to borrow. Likewise, your credit card rates and Home Equity Lines of Credit rates will likely move in direct proportion to the Fed's actions.

While a lowering of the Federal Funds Rate could eventually trickle down to the mortgage market, it doesn't happen instantaneously, and sometimes it doesn't happen at all. Why? Because mortgage rates are tied directly to 10-year Treasury notes. When the yield on the 10-year note goes up, mortgage rates go up, and when the yield goes down, mortgage rates go down.

It's possible for a lower Fed rate to eventually make its way to the mortgage market if investors react to the lower rate by buying bonds, and specifically the 10-year note. Doing so causes the price of the 10-year note to go up, and this in turn drives the yield - or rate - down. But it's important to understand that a Fed rate move never directly guarantees a mortgage rate move.

Having said that, there is one type of mortgage rate that typically does follow the Fed's rate moves, and that is ARMs, or Adjustable Rate Mortgages. If you have this type of mortgage, your rate is likely tied to the Prime Lending Rate, which is directly impacted by the Fed Funds Rate. But aside from ARMs, other mortgages are simply not driven directly by the Federal Reserve.

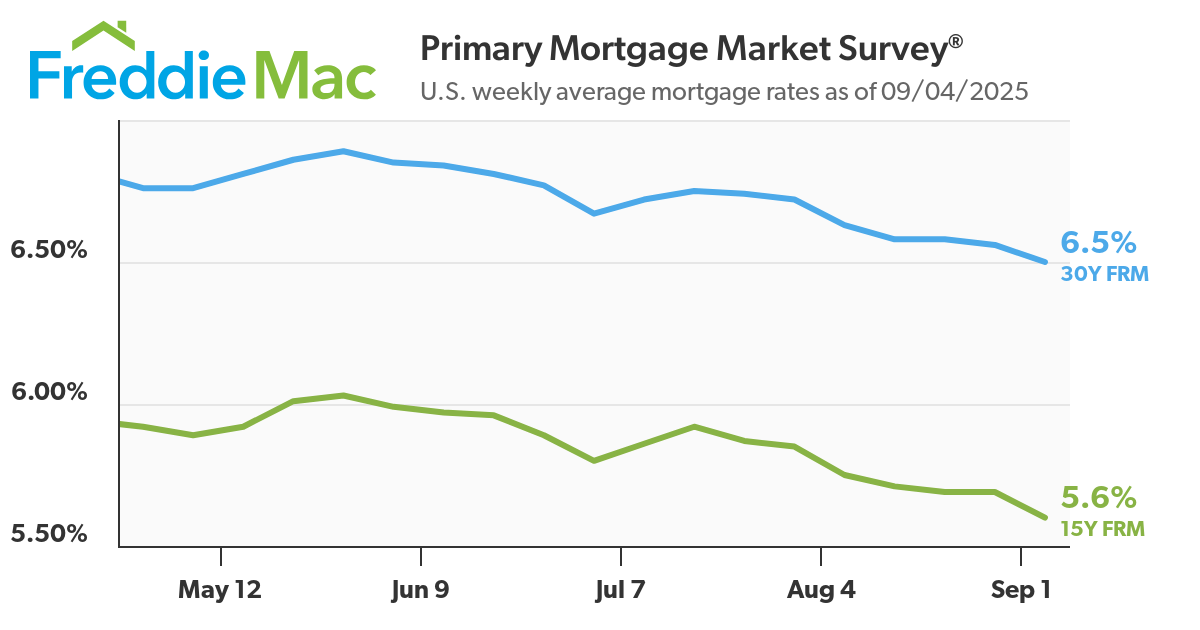

Mortgage Rates Have Already Dropped

What often happens in the case of a Fed rate cut is that the bond market anticipates it ahead of time. When the general feeling amongst investors is that the Fed is going to cut rates, those investors will often go ahead and start buying bonds in an attempt to get ahead of the curve. Again, this drives the price of bonds higher and, consequently, yields lower.

This appears to be what we have been seeing now for the last couple of months.

This mortgage rate chart shows that since the first of June, rates have been steadily declining. To be sure, not all of this decline is due to an anticipation of a Fed rate cut, but certainly over the last 3 - 4 weeks, there has been much chatter about a rate cut from every corner of the news world, and you can see that mortgage rates have continually declined over this period.

It is very possible that we have already seen all the mortgage rate decline we will see related to the anticipated Fed move. This is not set in stone, but in recent history, when mortgage rates dipped in anticipation of a Fed rate move, they didn't decline any more once the Fed actually adjusted interest rates.

Conclusion

The overarching message here is don't wait for a Fed rate move to buy or sell a home. If your only reason for waiting is because you believe mortgage rates will go lower after the Fed lowers the Federal Funds Rate, you are most likely wasting your time. Even if mortgage rates do fall a little more, they are unlikely to fall significantly once the Fed does lower rates - assuming they lower them at all.

And this brings up one more point. We don't even know for sure that the Fed will lower rates. While most economists and investors are anticipating a rate cut, they are not the Federal Reserve. If the Fed chooses to leave rates alone one more time, I could easily see mortgage rates heading back up as investors turn around and sell bonds to cash in on profits they may have made in anticipation of a rate cut.

The truth is, none of us knows for sure where interest rates are going, much less where mortgage rates are going. But one thing we can be certain of is that mortgage rates track 10-year Treasury notes. If you are concerned about mortgage rates and where they might head, your best bet is to keep an eye on Treasurys.

Meanwhile, if you are considering a move, you would be wise not to base your timing on a possible September rate cut.